“Price is what you pay; value is what you get.” – Ben Graham (2008 Berkshire Hathaway Performance Letter)

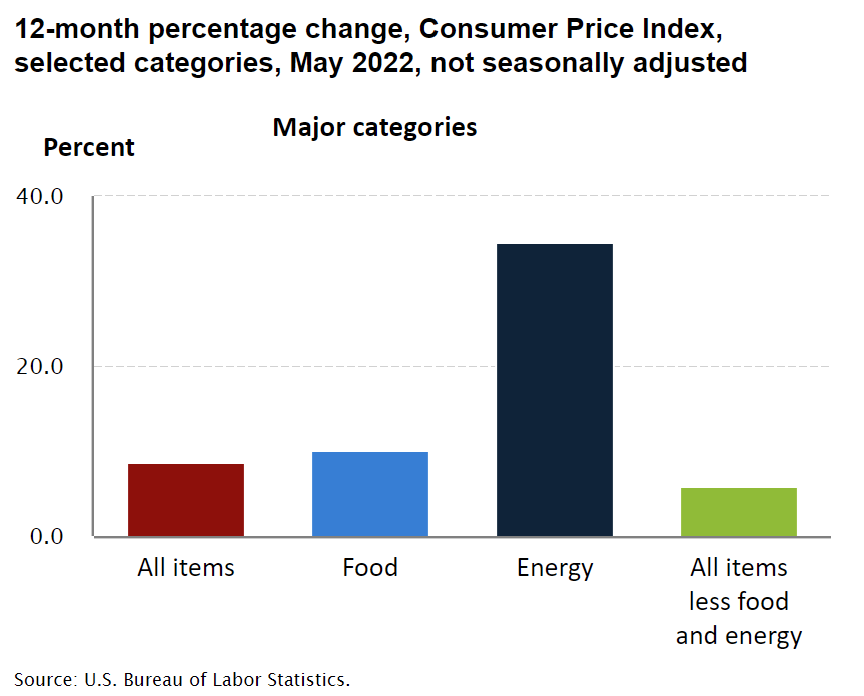

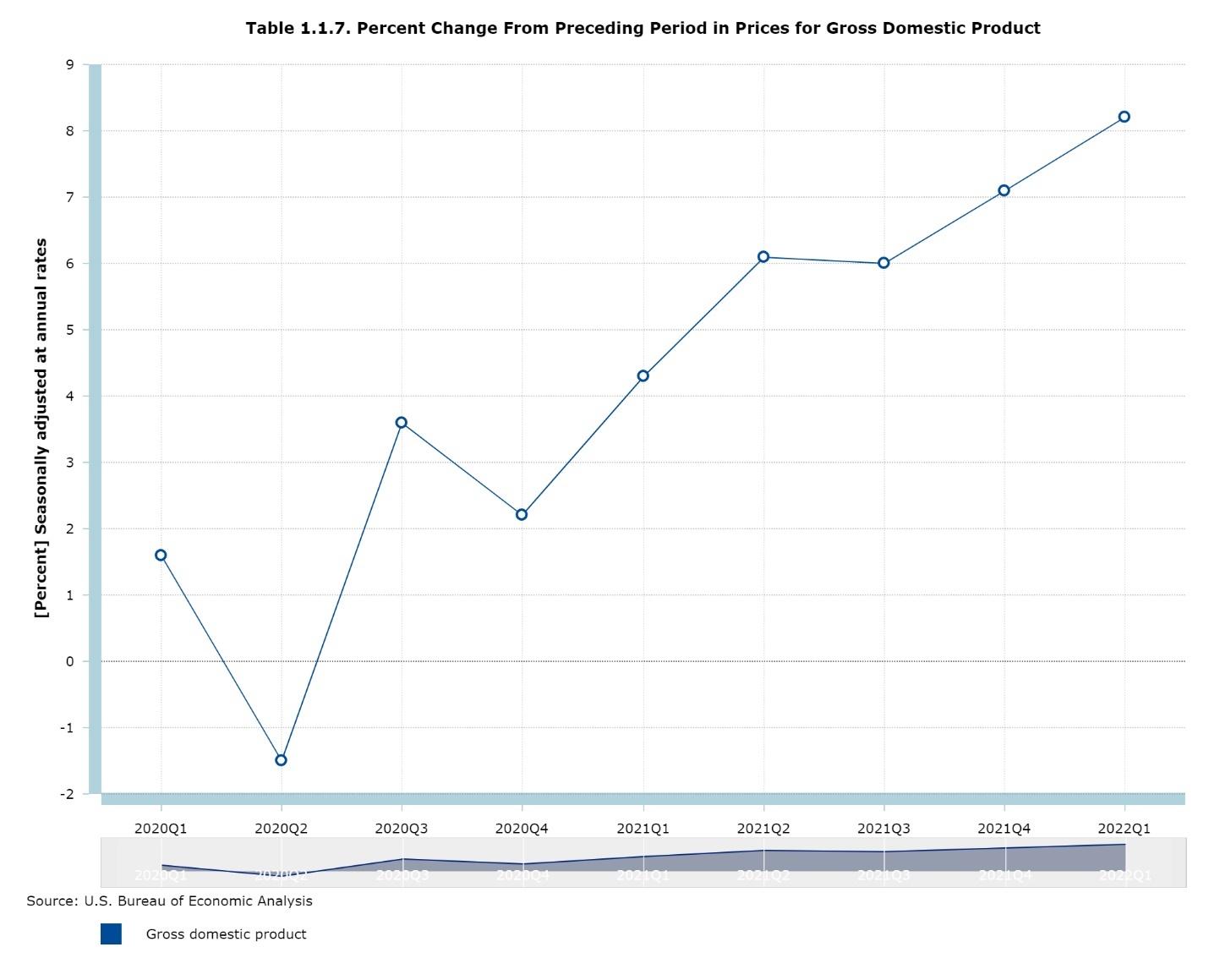

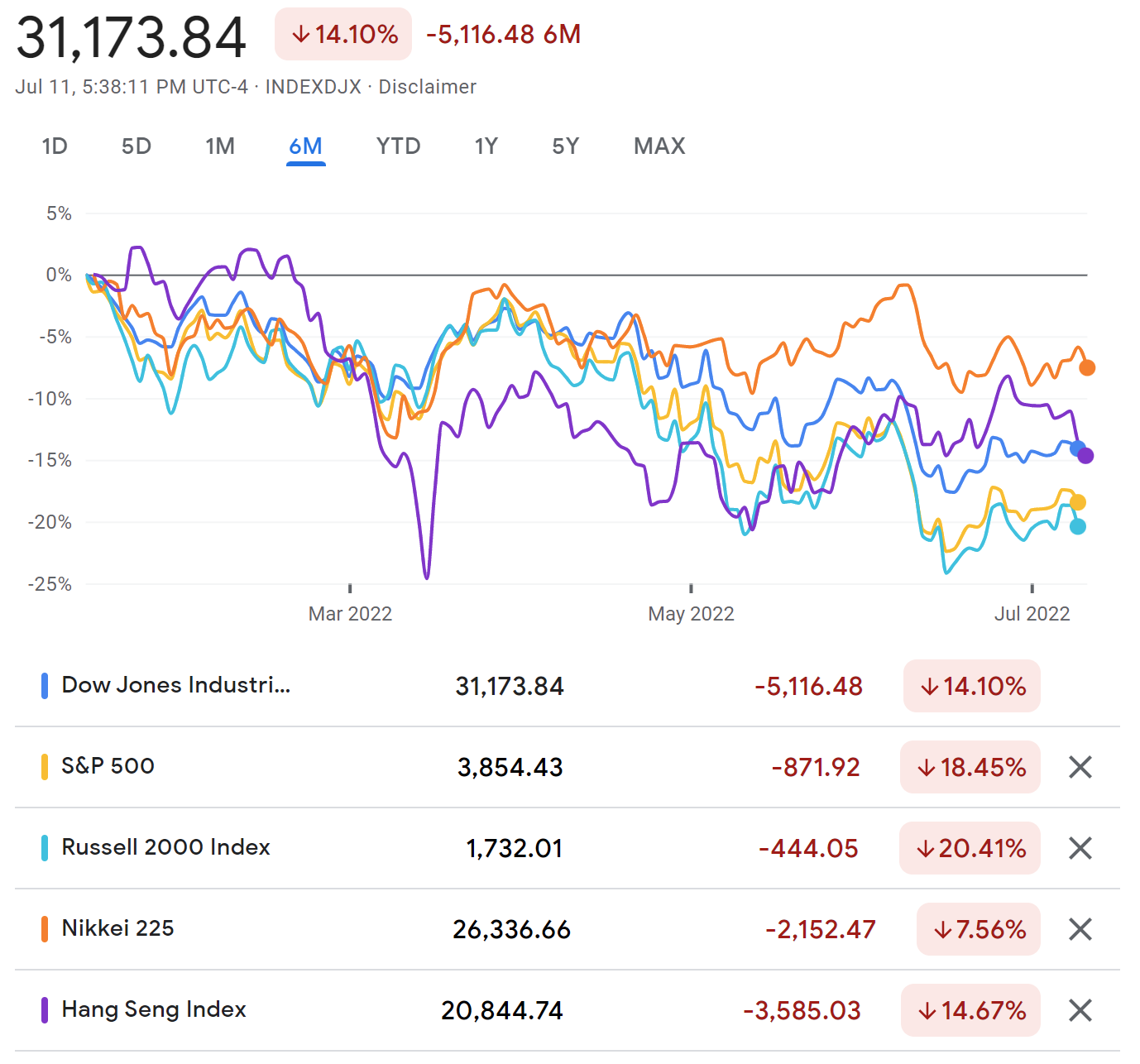

At the time of this writing, we are very much in a bear market. There is a ray of hope in the charts this week, but we are far from being out of the woods. The fallout of a global pandemic put the world on pause, and the subsequent bull-whip effect of latent demand has outstripped the capacity of the supply chain. The instability of the situation in Eastern Europe and its effect on food, oil, and other commodities has caused more than just uncertainty – it has resulted in absolute chaos.

In this highly charged political atmosphere, leaders of all countries are wrestling with inflation and the difficult challenge of implementing sanctions while dealing with their ramifications to our global network of interconnected trade.

You don’t need a Ph.D. in macroeconomics to recognize that the economy is fried. Prices of everyday essentials have skyrocketed around the world, and households are coming to grips with the cost of living increases.

Crypto’s Internal Battle

Macro isn’t the whole story, and while the past couple of years have shown a fairly tight crypto correlation to macro, we’ve had our own set of problems to deal with that have added fuel to the fire.

This cycle peaked in November 2021 with a total market cap of nearly $3 trillion before the dominos of an overleveraged system began to fall – beginning with Terra, and followed by 3AC, Celsius, and other centralized lenders.

Dropping to under $1 trillion, over two-thirds of the total value of crypto was erased in just a few months. The overwhelming hope and euphoria in November was intoxicating – the signs of a top were there, but the exhilarating ride blinded most investors. Innovation was ignored in favor of forks and DeFi casino games, which often ended in dramatic rug-pulls. We became numb to the overwhelming deluge of reports from Rekt.news. TradFi firms ventured further and further into DeFi and brought their old bag of tricks with them, saddling up with their biggest ally: CeFi lenders.

This disastrous duo used enough leverage to make Archimedes blush, moving the entire world of crypto on the fulcrum of false promises of solvency.

As these large funds looked to improve their returns beyond boring arbitrage practices, they ventured too far onto decaying ground by overexposing their funds to reflexive assets such as UST, and betting big on the risky GBTC trade. When these failing plays infected the funds, the following contagion rippled throughout many of the CeFi and TradFi groups.

This presented another opportunity for crypto degens, whose experience in hyper-volatile markets gave them the resilience needed to survive these nuclear conditions.

Arthur Hayes’ illustrative articles on this spectacular chapter in DeFi dive into the disastrous joint expedition by 3AC and CeFi lenders.

Additional sources on the Luna-3AC-Celsius carnage:

- Voyager Digital Bankruptcy 3AC

- Celsius Partner Details Inner Workings of Ponzi Scheme in Lawsuit

- Celsius Lost $350M of Client Funds From ‘High-Risk’ Levered Trading

- Zhu, 3AC, & Starkware

- Crypto Crash Drags Lender Celsius Network Into Bankruptcy

- Three Arrows Capital Creditors Lent Bankrupt Fund $3.5 Billion, Court Documents Show

- How Three Arrows Capital Blew Up and Set Off a Crypto Contagion

Battle-Tested

While the lack of transparency on the CeFi front revealed the flaws of a trust-based system, DeFi protocols continued to operate smoothly. On-chain lending protocols forced liquidations, preventing lenders from becoming insolvent.

And through the market apocalypse, builders are continuing to develop and expand the use-cases for crypto. For example, MakerDAO is attempting to bring DeFi loans deeper into the mainstream with a proposal to offer a $30M loan to Societe Generale, the third largest bank in France, to refinance $40M worth of bonds encompassing home loans and other corporate obligations.

Many of those who made deals off-chain and behind closed doors fought to enforce agreements made on paper through desperate late-night Telegram messages. The litigation will require months of work to resolve these insolvent accounts and unpaid debts. The death rattle of the fallen will continue to echo across the battlefield for months to come as the full extent of the fallout is revealed.

Meanwhile, those that have embraced on-chain agreements enforced by code have soldiered on.

The Value of Tokemak

The pieces are falling into place:

- DeFi is proving itself to be a more reliable, transparent, and efficient technology.

- The projects and protocols embracing true decentralized finance through smart contracts have continued to operate as intended throughout the high market volatility .

- Web3 is still a new and rapidly expanding space.

- Deep liquidity is critical for this space to continue to grow and flourish.

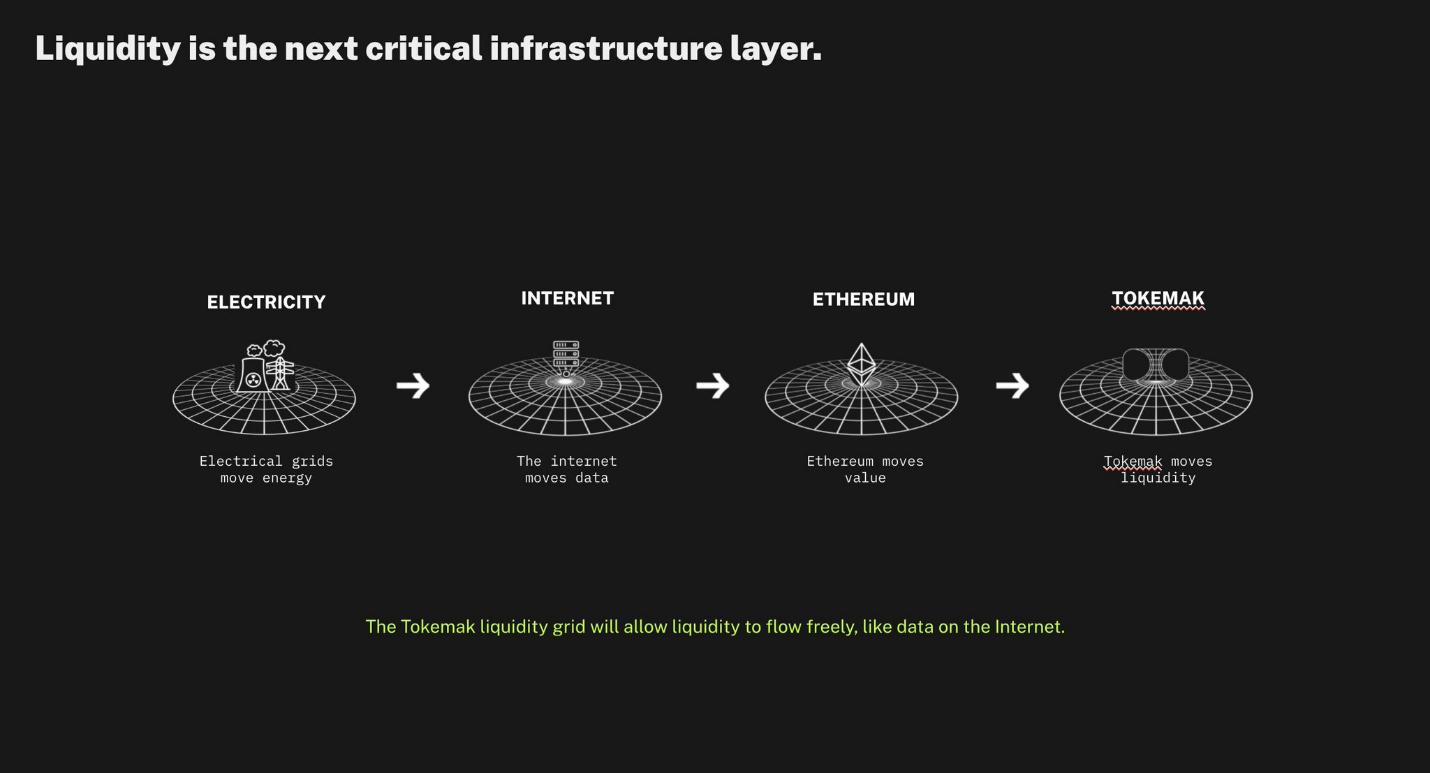

Tokemak offers a solution to a major constraint DeFi and Web3 have faced over the years: liquidity. Sufficient liquidity is what allows fast, efficient exchanges of crypto assets, which is critical in DeFi. Low liquidity results in high amounts of slippage, and increases friction in systems designed for free-flowing exchange of value.

Tokemak’s vision is to provide a deep source of liquidity for the wide breadth of assets across web3.

- What is Tokemak?

- Sustainable Liquidity for DAOs - Tokemak: The Utility for Sustainable Liquidity

- Tokemak Pilot Manual

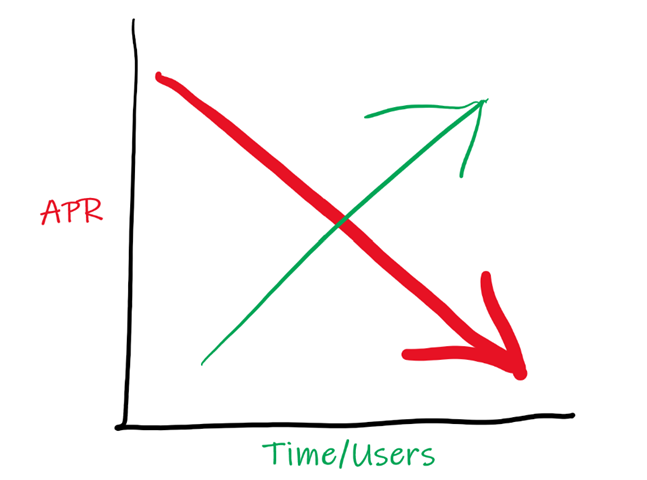

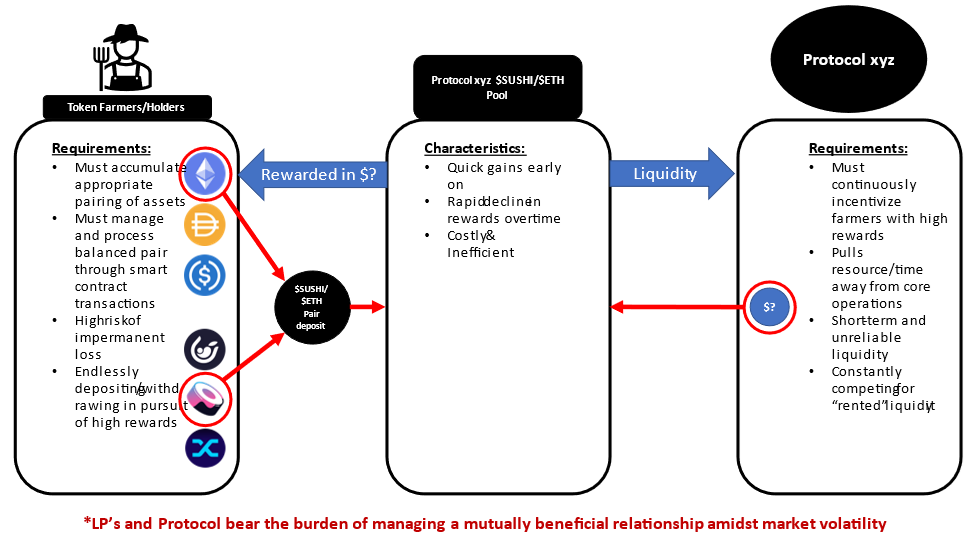

Tokemak alleviates the need for costly inflationary pools that supply an unreliable source of liquidity and attract mercenary capital. Protocols have relied on unsustainable incentive mechanisms to encourage token holders to provide liquidity to AMM pools. Inevitably, liquidity providers flood in to farm the rewards, diluting the yield, while continuing to dump the earned tokens – creating constant sell pressure for the protocol’s native asset. Then, like a swarm of locusts, they migrate to the next farm.

Tokemak reduces friction by oiling the cogs of DeFi, improving efficiency and reducing the need for short-lived solutions.

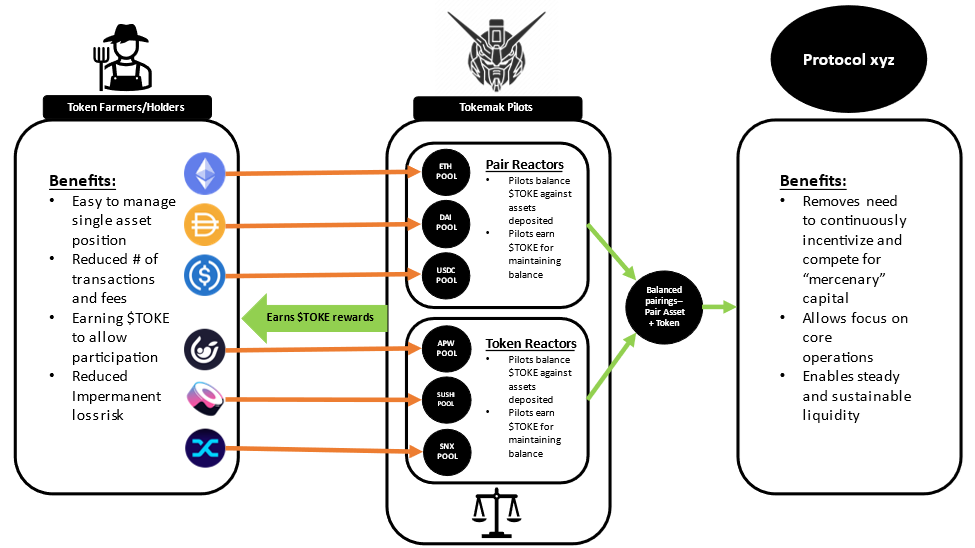

The Benefits of Tokemak

For Protocols

- Reduces emissions.

- Reduction in sell pressure.

- Steady and sustainable source of liquidity.

- Reduction in pool management costs.

For Users

- Reduced gas fees.

- Impermanent loss mitigation.

- Easy to manage single staking positions for a variety of assets.

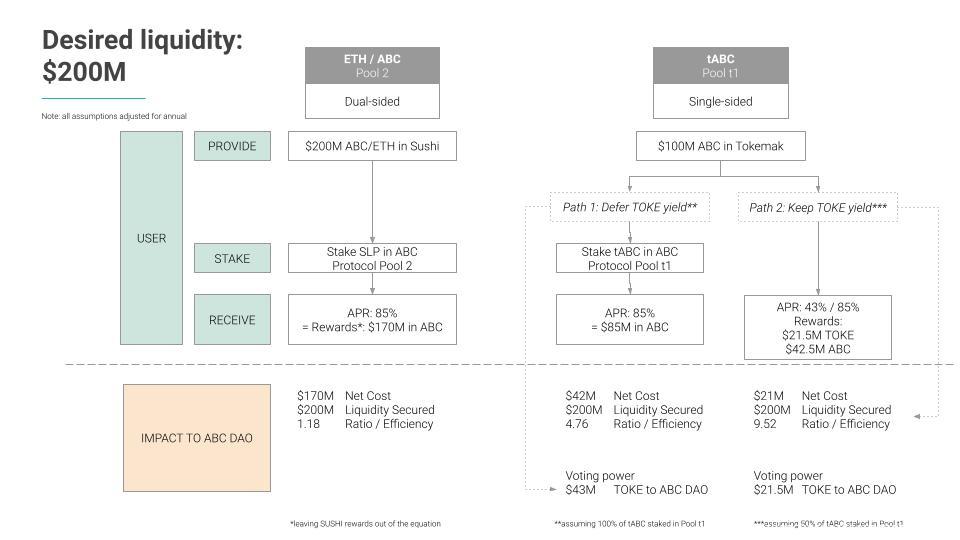

The ability to efficiently transfer value is critical to web3, and Tokemak offers a cost-effective way to source the liquidity needed to accomplish this across the web3 space. The Cost of Liquidity demonstrates Tokemak’s potential to reduce the cost of sourcing $200M in liquidity from $170M to under $42M. This level of improvement can have an immediate positive effect on protocols, since they are able to allocate more resources toward their primary goals rather than be burdened by the effort and cost of market making.

As Tokemak continues to ignite new Reactors, it can offer more opportunities for idle, unproductive tokens.

The largest benefactors of Tokemak are DAOs, rather than end-users; however, with current market conditions and price action, there are opportunities for all. TOKE holders are able to direct an outsized amount of liquidity-per-dollar, which creates significant opportunities for utility. Tokemak’s upcoming ACC mechanics will allow holders to stake TOKE and earn a share of protocol revenue.

An Analysis

- Competition

- Bancor’s liquidity service has been tested harshly during this period of market volatility. The protocol’s impermanent loss mechanism entered a “death spiral” due to the mint-to-cover strategy, forcing the team to halt its IL mechanism. Source: Bancor Halts Impermanent Loss

- Tokemak is very difficult to fork due to off-chain secret sauce and sticky protocol-owned assets.

- New Entrants

- While the barrier to entry in web3 is typically low due to its open source nature, sourcing liquidity and managing impermanent loss is incredibly complex and time-consuming.

- Suppliers

- Tokemak is built to be symbiotic with AMMs and liquidity providers, so incentives are aligned, mitigating the risk of suppliers competing against Tokemak.

- Customers

- The utility of TOKE also creates stickiness as DAOs grow their governance power from rewards, further increasing their control over liquidity across Reactors.

- Alternates/Substitutes

- The current standard for sourcing liquidity is dual-sided liquidity pool farming which is costly, inflationary, and exposes LPs to significant risk.

- Olympus Pro bonds offer a compelling mechanism for a protocol to accumulate its own liquidity, but are not a one-size-fits-all solution and largely depend on intrinsic demand for the protocol’s native asset.

Tokemak has excellent internal and external alignment in the web3 ecosystem. It supplies a valuable and necessary service to a wide variety of protocols: sourcing liquidity at a low cost with minimal overhead, while having a direct influence in deciding where to direct liquidity. Stable and sustainable liquidity would benefit the ecosystem as a whole by helping reduce the volatility we see in the space, while also offering protocols an option to minimize inflationary liquidity mining programs that have plagued crypto since the start of DeFi Summer.

For more insight into the history of liquidity, see our previous articles:

The Curve Wars have been a hot topic in the fight for stablecoin dominance, with protocols racing to accumulate CRV in order to incentivize deep liquidity and strengthen their stablecoin’s peg. Tokemak’s integration with Curve makes it a valuable source of liquidity, and some of the largest players in the Curve Wars are acquiring large amounts of TOKE in preparation for the next stage of the broader Liquidity Wars.

Where We Stand

Tokemak is still in its early stages, with a limited number of Reactors and guarded liquidity deployment. Regardless of these scaled-down operations and the current bear market, the protocol continues to generate significant income, and is on-track for revenue to exceed emissions.

Additional value drivers are on the horizon, including the following:

Exaverse

- Exaverse is an upcoming NFT game modeled on the Tokeverse with its own EXA token and integration with the Tokemak contracts.

Membrane

- Membrane is an upcoming OTC and credit-layer protocol being designed by Liquidity Wizard. It is expected to directly integrate with Tokemak as a liquidity direction venue.

CitadelDAO

- C.o.R.E. participants have been whitelisted to take part in CitadelDAO’s launch. This project is a sub-DAO of Badger and seeks to increase BTC’s utility within DeFi.

HiddenHand

- HiddenHand is a protocol focused on increasing governance influence through bribes. DAOs may incentivize votes for Reactors during C.o.R.E. as well as general liquidity direction.

Web3 requires the efficient transfer of value across chains and between assets. In low-liquidity environments, large swaps cause volatile price movements and losses due to slippage. Incentivizing deep liquidity through mining programs has already proven to be an unsustainable endeavor, and few solutions exist to solve this problem. Tokemak, much like its namesake, aims to power this fundamental need across DeFi.

Crypto as a whole will survive to see a 5th cycle, but not all projects will – finding core value amid the wreckage is key to positioning for the next bull run.

☢️❄️ Stay Frosty ❄️☢️