I return to you from the fields with another report on the Liquidity Wars. Shortly after my last report, The Liquidity Wars: Impact, the cryptoverse was rocked by the TERRA/LUNA collapse – along with the fall of Three Arrows Capital (3AC). The carnage and crypto winter have descended upon us. Bitcoin is struggling, while Ethereum surmounted a critical milestone: The Merge, which introduced more volatility on its own. The transition from Proof-of-Work to Proof-of-Stake caused chaos as some players attempted to cling to Proof-of-Work and traders tried to take advantage of the split.

There will certainly be more meteoric rises and market-shaking collapses to come. Liquidity will play an essential role in these ups and downs, and DeFi and web3 are still wrestling with sustainable, reliable liquidity.

As I stride through the fray of the web3 battlefields, everyone is tired and almost everyone is down. In these moments, many protocols will fail the test of a down cycle. Yet what do I see?

Across the cryptoscape, the black flags of Frax appear. Lending, swaps, staking, indexing, and bridging, all adorned with the black banner. The results of quiet but determined building are suddenly clear: there is a powerful force surfacing throughout DeFi.

First Things First

If you are new to the Liquidity Wars, you have a lot of catching up to do. There are a lot of great articles documenting these wars, with most centering around Curve and Convex Finance. The preceding articles in the Tokebase Liquidity Wars series provide plenty of additional resources on DeFi’s continuous contests for liquidity:

For those of you with the attention span of a typical CT degen, I’ll summarize. In the beginning, protocols sought and flaunted their total value locked (TVL). In order to achieve high TVL and liquidity, they offered farming incentives to liquidity providers. This led to competition amongst the various protocols and launched mercenary capital: farmers seeking the highest returns. It presented the problem of unreliable and costly liquidity and often resulted in farmers dumping the rewards, which in most cases were that protocol’s governance token. It was costly, inflationary, and perpetuated sell pressure – which, by the way, really hurts in down cycles like the one we are currently experiencing.

Along came Curve Finance (token: CRV), a stableswap protocol that would implement gauges for CRV holders to vote/direct CRV emissions to pools on its platform. The TVL Wars expanded into the CRV Wars.

Protocols realized that by hosting their pools on CRV and having the CRV emissions/inflation voted toward their pools, they could gain a more efficient source of liquidity. Votium launched to allow protocols to bribe CRV holders for their votes/emissions directing. Convex (token: CVX) quickly realized how lucrative and powerful CRV and its gauges were. Convex made a decisive early strike to become the largest and most influential CRV holder.

The mechanisms Convex put in place led to the CRV Wars becoming the CRV/CVX Wars. The two have almost become synonymous at this point, but just remember that in the end it’s really about those coveted CRV emissions from the Curve gauges. With Convex becoming the most influential holder of CRV, protocols and DAOs began accumulating CVX. The benefits of controlling the stableswap protocol’s governance token were so lucrative that it led to the creation of many additional CRV/CVX focused efforts from protocols like [REDACTED]’s Pirex, AladdinDAO’s Concentrator, and StakeDAO.

While the CRV/CVX Wars played out, yet another battleground was emerging, as Tokemak began rolling out a scaled launch of its liquidity deployment. This offered protocols a more cost-effective and easily managed source of liquidity, while simultaneously tying directly into the CRV/CVX mechanics. Thus began the TOKE Wars, which are still on relatively fresh battlegrounds. Further discussion of Tokemak and the value it offers can be found in our Fourth Impact article.

The Liquidity Wars were rapidly evolving and growing more complex. Then, almost as quickly as they took off, progress was brought to a crawl or possibly even a halt as the TERRA/LUNA and 3AC events crashed crypto in tandem with macroeconomic events. That brings us to present day conditions: battered, bloody, and tired, the Liquidity Wars combatants continue their contest in the frosty crypto winter that has descended upon us.

The Empire of Frax

While many other protocols caught the headlines over the past year, Frax has flown somewhat under the radar. The Frax team seems to be taking the “our product speaks for itself” approach. If you haven’t been actively looking, you may have missed Frax’s product expansion and impressive growth. Frax has been heads-down, building an infrastructure for DeFi right beneath our feet.

Let's dive into the Frax empire's growing power and influence in these wars.

CRV/CVX Influence

We’ll begin with the most heated and recognized battlegrounds.

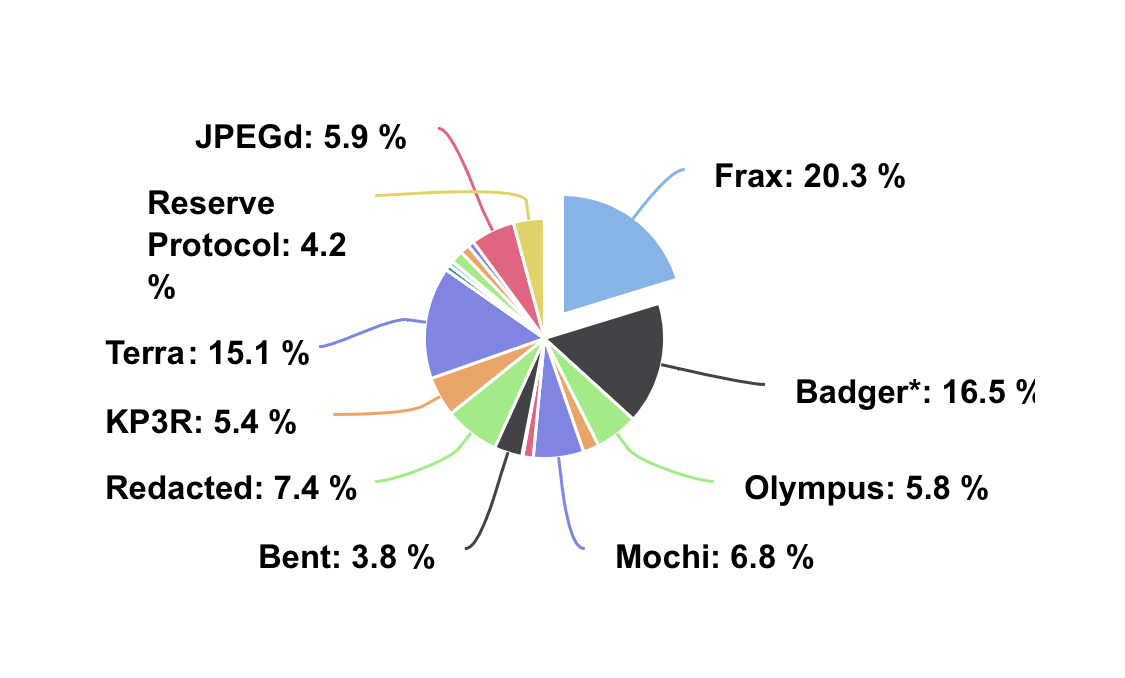

Of the 24 DAOs accumulating CVX, Frax is the largest, holding 20.5% of DAO-owned CVX.

It’s also worth noting the combined influence of protocols that have very close relationships with Frax. [REDACTED] has a strong tie through the Hidden Hand integration for Frax. OlympusDAO has been a longtime partner and source of bonding activities. BadgerDAO’s sub-DAO, CitadelDAO, offers an ICO allowlist for Frax holders. In short, Frax has a strong influence on CVX – and therefore CRV – that could be amplified by its close partners.

Tokemak Influence

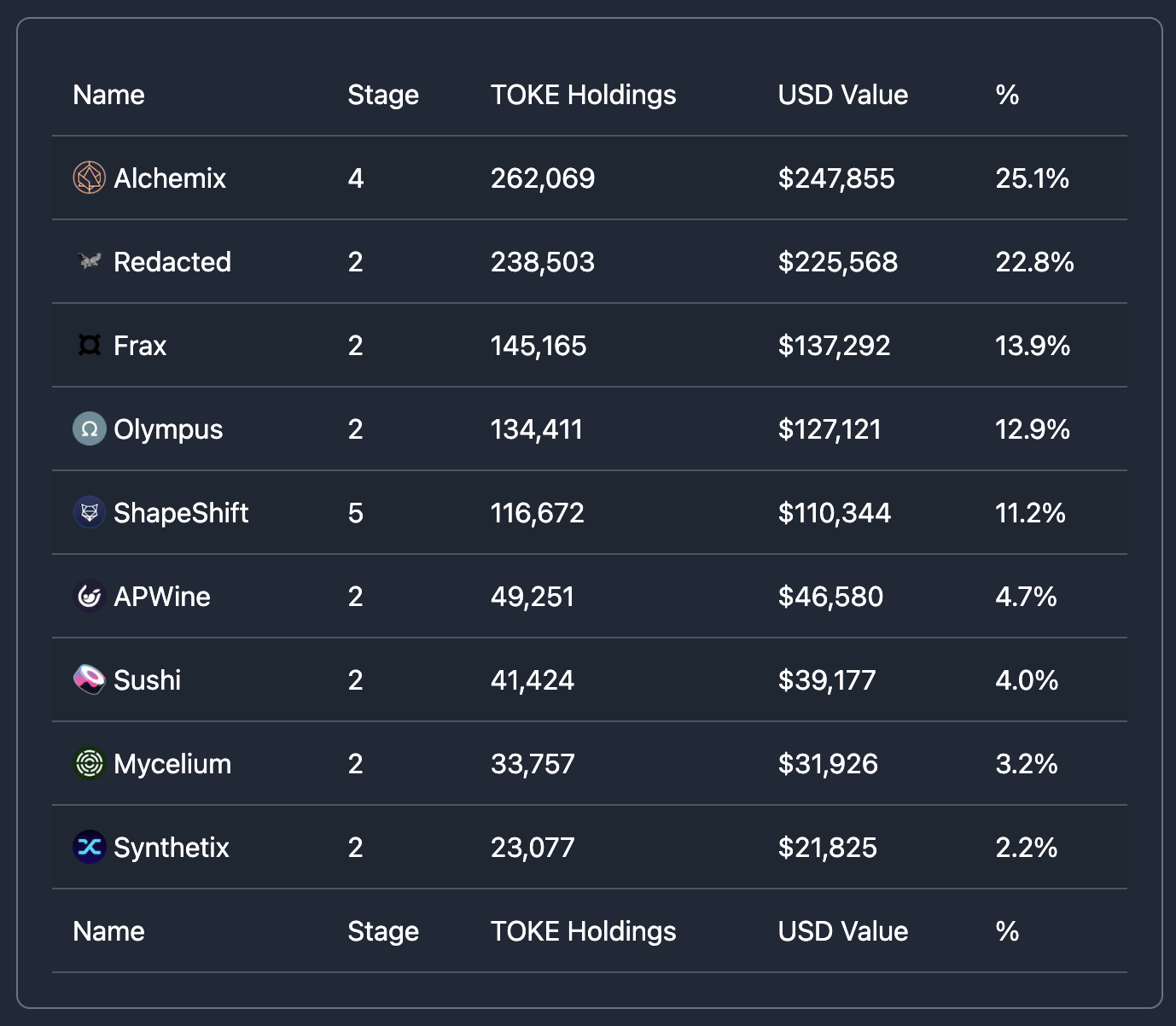

Frax has the third-largest DAO holding of TOKE, and again we see its close friends OlympusDAO and [REDACTED] adding to that influence. As Tokemak grows, Frax will not only benefit in efficiently sourcing liquidity; it will also have a strong influence in governance and directing liquidity, much like its current powerful influence over the CRV gauges.

Convex Interest

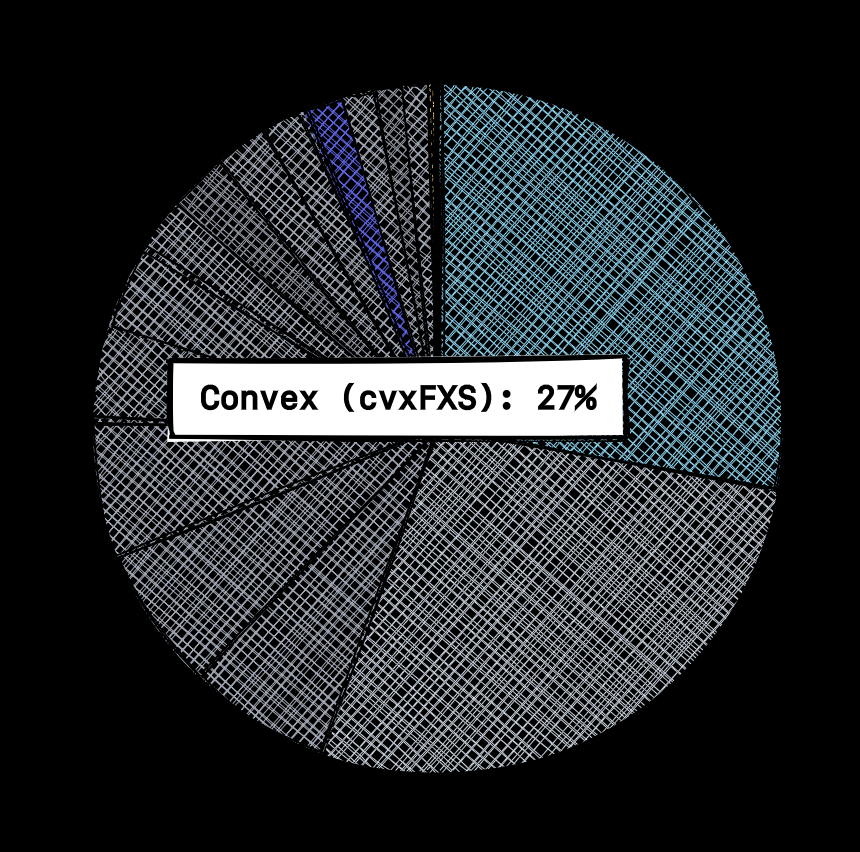

Convex Finance is a powerful force in DeFi that demonstrated their foresight when making some of the earliest moves in the CRV Wars. It’s worth noting that they are the largest holder of FXS: 27% of supply.

What do they know? 🤔

The Takeaway

Frax holds enormous sway in the liquidity wars, and has also positioned itself as a key piece of infrastructure. Convex has recognized this and is trying to replicate the success it had in the CRV wars by quickly taking a leading position. Even more interesting is the combined influence wielded by the gathering cohort of protocols and DAOs with a focus on solving DeFi’s liquidity problem. Take one last look at the names above: [REDACTED], OlympusDAO, Tokemak, Curve, Convex, and even Rook all have close relationships, if not some level of interoperability with one another.

A Basic Overview of Frax Finance

Frax has a very complex ecosystem, and it’s well worth your time to read through their docs. However, for the sake of this article, I’ll run through the basics of what Frax currently offers and how they operate.

FRAX

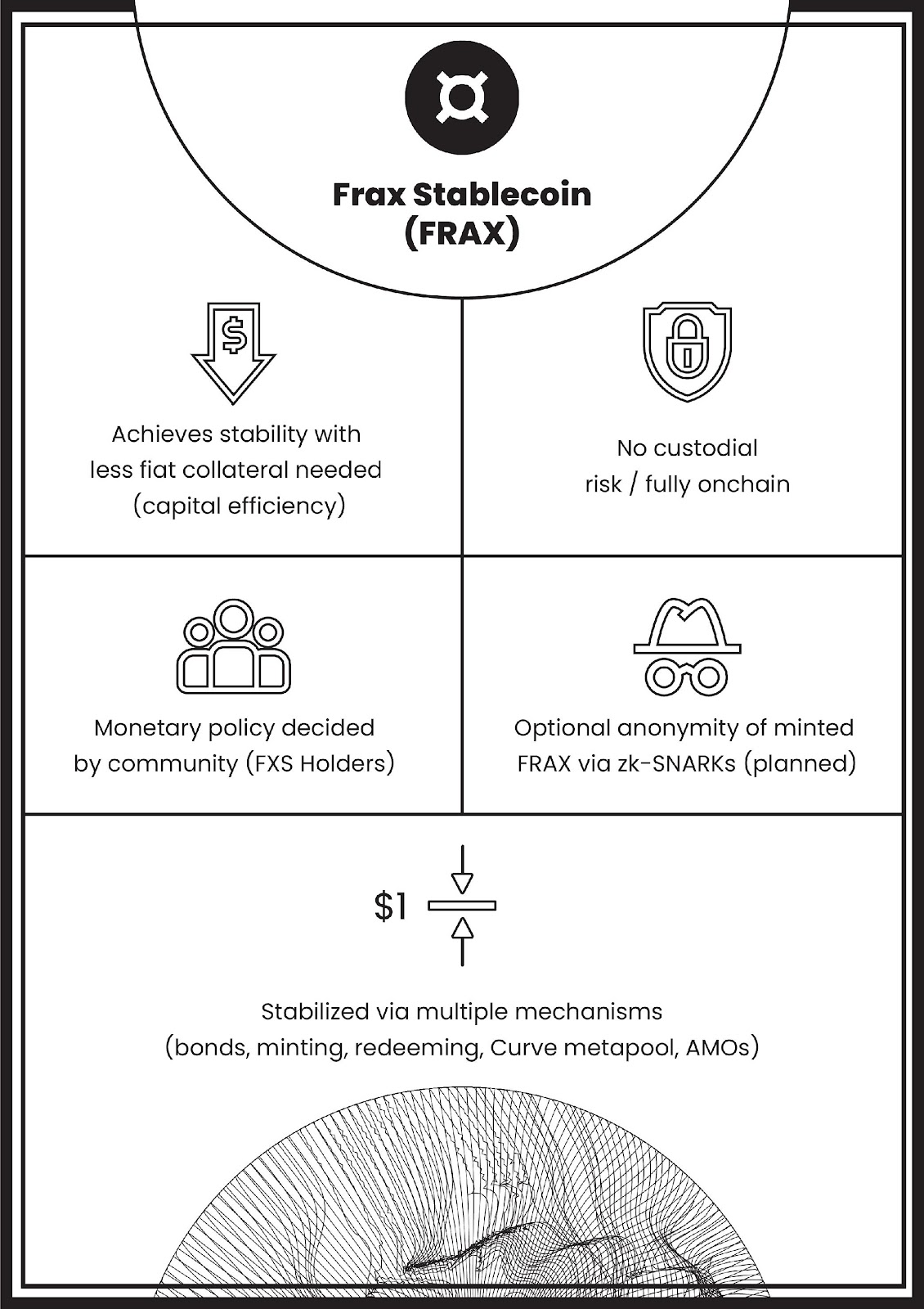

FRAX is the algorithmic fractional stablecoin at the heart of Frax Finance. This stablecoin is unique in that a percentage of the supply is backed, but its algorithmic feature allows it to scale beyond its collateral. Frax refers to this as the Collateralization Ratio or CR. FRAX will scale with the market's demand, so if the market has no appetite or trust in FRAX beyond its collateral, it will likely remain at or near 100% collateralized. If the market is confident and comfortable with FRAX’s algorithmic feature, then supply can expand rapidly to meet demand.

Frax is essentially incorporating the benefits of both collateralized and algorithmic stablecoins. Collateralized stablecoins are able to maintain a tight peg and are highly trusted, but they are slow to scale and tedious to manage. Algorithmic stablecoins can offer high scalability, but also are typically more volatile.

This new and dynamic approach makes FRAX DeFi’s ideal stablecoin. It captures the core needs of stability, scalability, trustlessness, and decentralization.

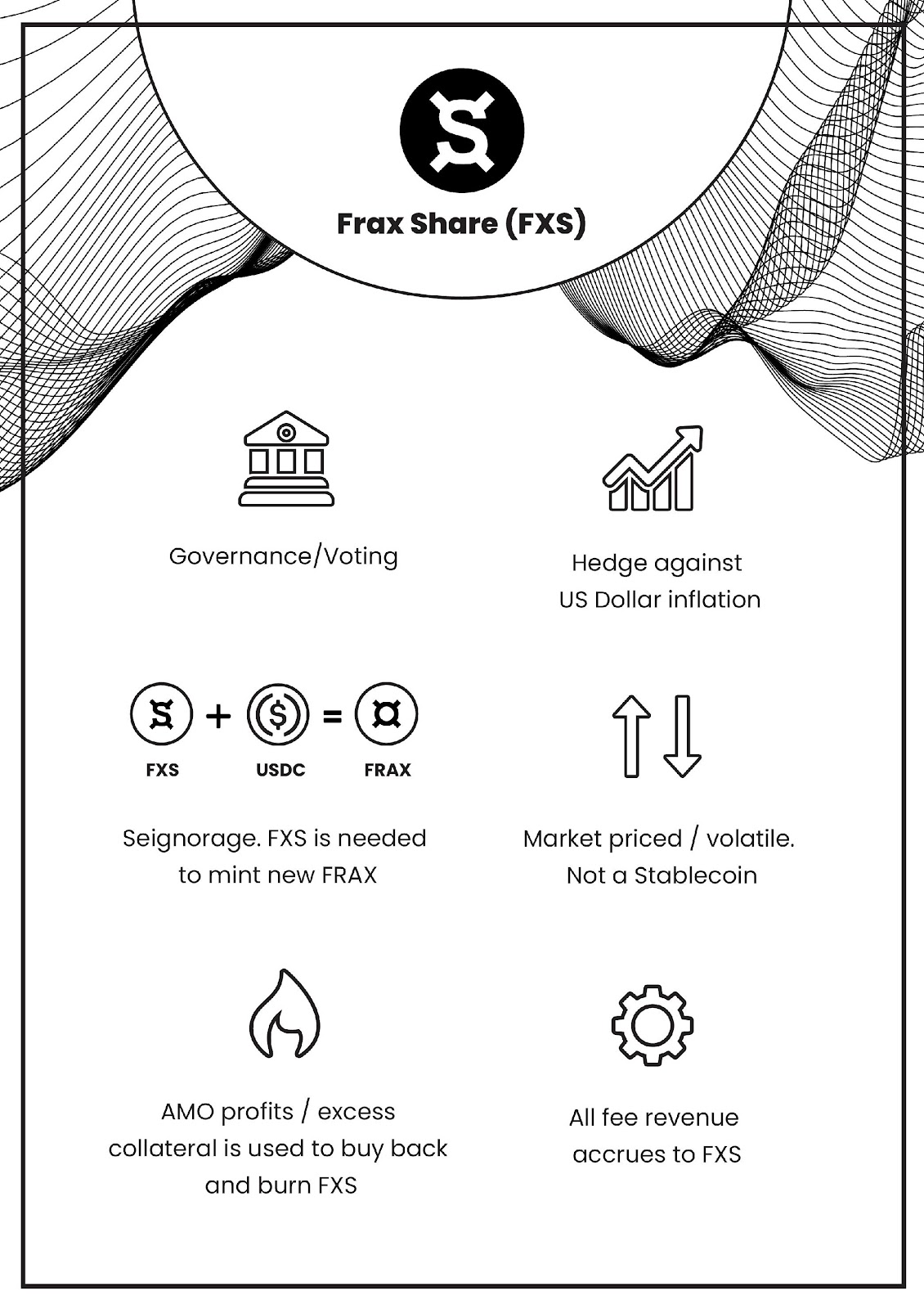

FXS – Frax Shares

FXS is the overarching governance token of the Frax ecosystem. FXS can be locked for veFXS, which grants voting power and rewards from fees, revenue, and collateral value.

FPI – Frax Price Index

FPI takes an innovative approach to addressing inflation by pegging to the U.S. Consumer Price Index.

FPIS – Frax Price Index Shares

FPIS is a governance token specific to the FPI product and its performance. FPI can also be locked for veFPIS. One important note is that veFXS holders also receive a portion of the benefits of FPI’s performance.

Fraxswap TWAMM – Time-Weighted Average Market Maker

Another unique feature to Frax, the TWAMM allows for the capability to process long-term orders and execute large orders efficiently. This short description doesn’t do this innovation justice – the description of its inner workings and benefits are worth a read in Frax’s docs.

AMO – Algorithmic Market Operations

The AMO is the driving force behind Frax Finance operations. It is responsible for managing the re-collateralization and de-collateralization per the current CR (Collateralization Ratio). It also manages FXS value accrual (FXS burns for fees, unbanked FRAX, and extra collateral).

Frax Gauges

Inspired by the Curve Finance gauges, Frax has its own gauges in which veFXS holders vote to direct emissions toward various pools on Frax. [REDACTED]’s Hidden Hand operates similar to Votium in that veFXS holders can be bribed to vote toward certain pools.

FraxBP

The Frax Base Pool is a FRAX-USDC pool on CRV which is a major benefit to both CRV and Frax, especially with the latest developments creating a positive sum flywheel such that emissions on both sides are being efficiently used instead of sold.

FraxBridge

Frax hasn’t confined its campaign to just Ethereum. Frax has a unique bridging mechanism allowing users to interact across chains including Polygon, Avalanche, and BSC.

Fraxlend

The latest release from Frax brings them into the DeFi lending market.

Frax Staked ETH – frxETH

Frax also has a soon-to-be-launched service allowing users to stake ETH with Frax, similar to offerings from Lido and Rocket Pool.

Show Me the Numbers!

Complex whitepapers are all well and good, looking impressive and making our eyes glaze over as we assume the party responsible for all this gibberish must be a genius. Of course, an idea or concept is one thing, but can you prove that it actually works and is truly generating value rather than hype?

Let’s look at how Frax has performed over the past year.

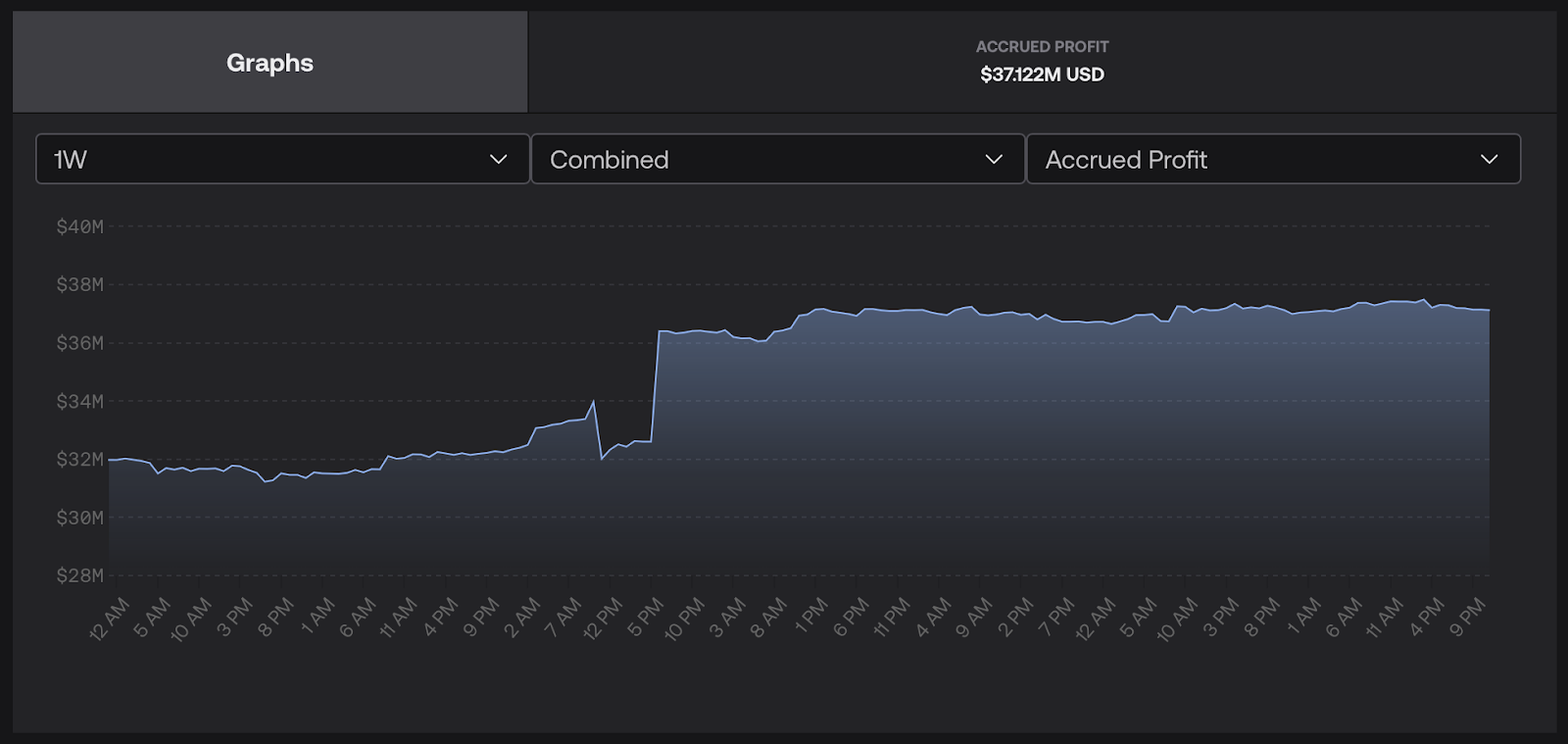

Currently Frax sits at over $37M accrued profit. The chart above depicts the rise and fall of its profitability, which aligns with the general events listed earlier. The rise started last October as DeFi and crypto hit mania levels; then a decline began in May, as TERRA/LUNA collapsed and the 3AC contagion spread.

Despite that, Frax has shown resilience and is resuming a steady climb back up. This is being driven by its Collateral Investor function whereby idle USDC is used to farm yield. An important consideration here is that ~$32M of the accrued profit is attributed to this conservative strategy. The newer initiatives have not yet had time to reveal the full impact and benefits they will bring to the Frax community.

Looking Forward

Frax’s performance is impressive, especially considering its resilience in the current downturn. The fact remains that we have yet to see what Fraxlend and ETH staking will do for Frax. To get a sense of the impact these new services might bring, let’s look at current leaders in these respective categories.

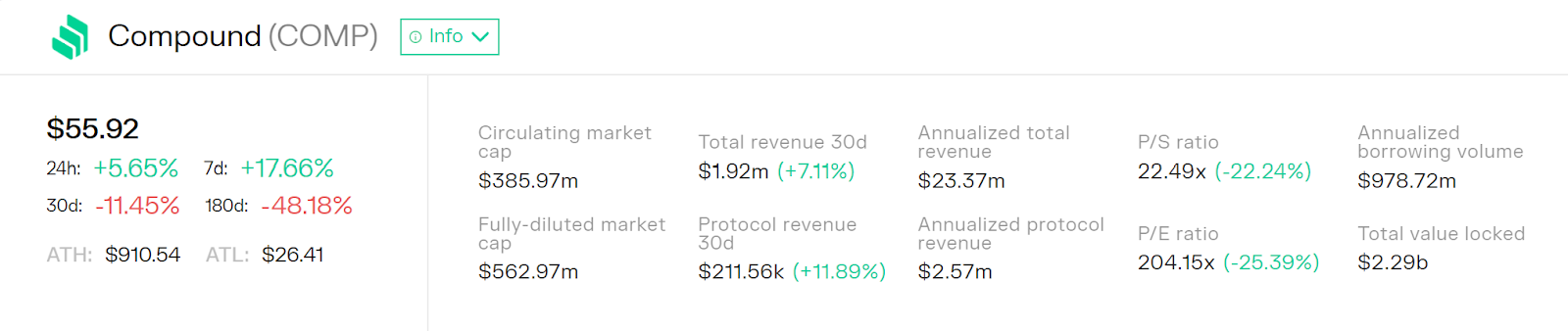

DeFi Lending

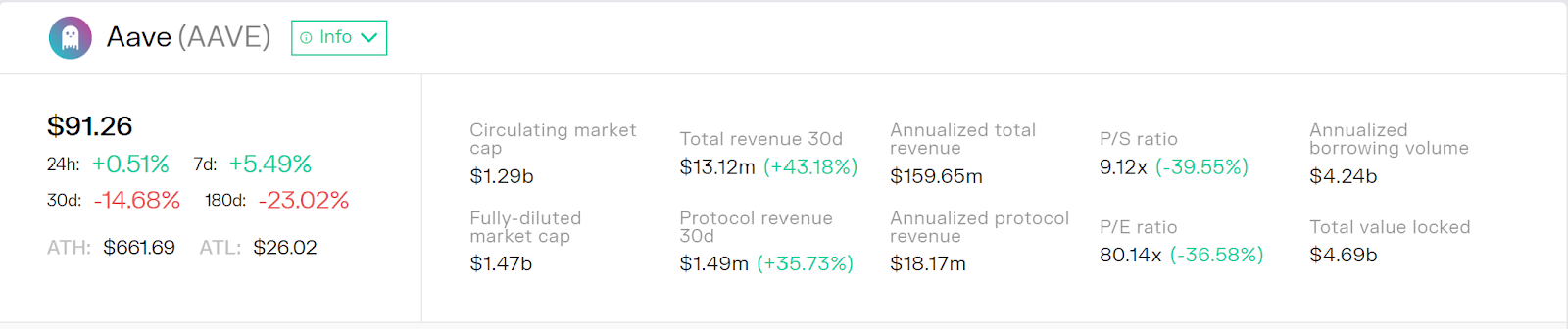

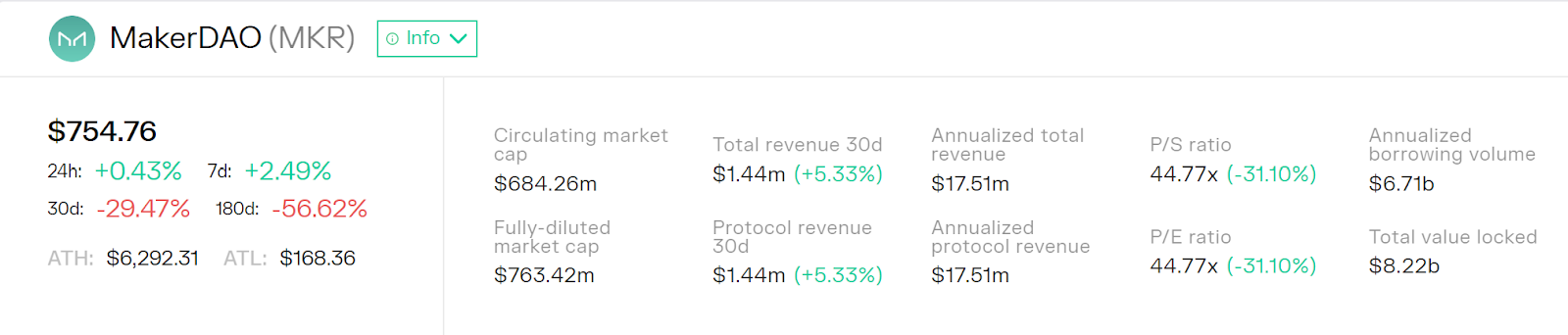

In DeFi lending, Aave, Compound, and MakerDAO have been long-standing leaders.

The charts above re-emphasize that borrowing and lending have always been DeFi’s bread and butter. Despite the bear market, all three protocols show healthy earnings, and are undervalued when evaluated strictly on performance. Both the risk associated with crypto as an emerging market/new tech and negative sentiment from macroeconomic events are pushing these prices down.

All that said, Frax’s FXS token currently sits at ~$325M circulating market cap and ~$67M in circulating supply, with accrued profits currently at $37.11M. That’s prior to Fraxlend placing Frax Finance as an additional option for DeFi users to consider when engaging in lending and borrowing.

Frax doesn’t even need to beat out Aave or Maker for top lending protocol to benefit enormously from entering this category. The ecosystem Frax has established will boost its appeal to users, even if simply through convenience. Borrowing and lending present an excellent use case for DeFi, and the current rising rates in traditional finance may make DeFi offerings much more enticing.

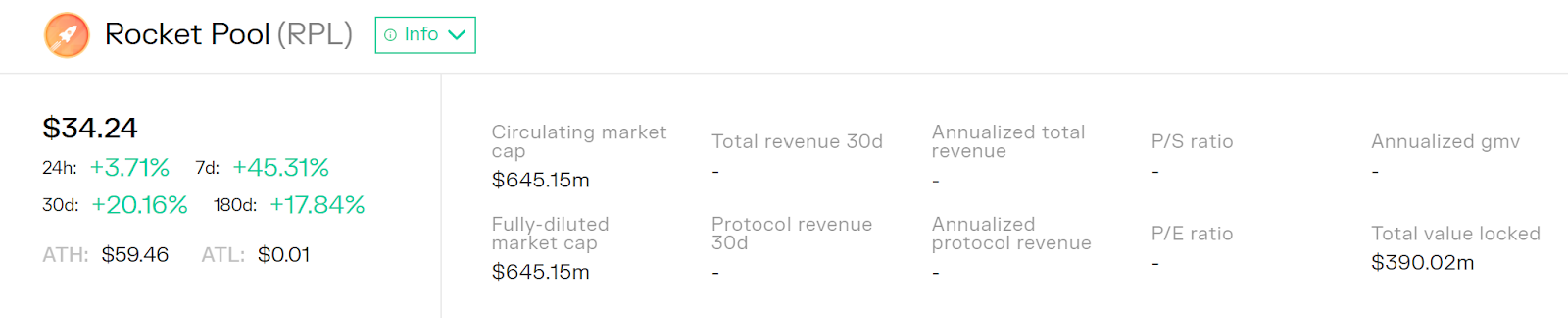

ETH Staking

When it comes to ETH staking Lido has an overwhelming majority of the market, with Rocket Pool being the second largest share.

With its dependency on the success of The Merge and the relatively short time frame it has been in place, it is uncertain just how significantly ETH staking could increase revenues. While it may offer sizable rewards, at minimum it will draw more value and users into the Frax ecosystem. More users, more transactions, more fees, and more attention: Frax has made another brilliant move in what appears to be a strategy to offer DeFi users a comprehensive protocol from which to proactively manage their assets.

The Great Frax-spansion

Frax has positioned itself as a strong contender in the Liquidity Wars and a powerhouse across DeFi. The Frax team has been building at an impressive pace, approaching each product or service with their own unique mechanics. Time and trials are still needed to learn just how strong a competitor Frax and its offerings can be in DeFi.

It is said so often it is almost meaningless, but we truly are early in crypto, web3, DeFi, and any other term referring to the use of blockchain technology and digital assets. Frax has built a wide array of opportunities for users to manage their assets actively and efficiently. Whether you are currently using Frax or watching from the sidelines, you will hear more about Frax’s impact in the space as their influence continues to spread.

As always,

☢️❄️ Stay Frosty ❄️☢️